This page provides guidance and optional templates to assist grantees with transferring CDBG-DR and CDBG-MIT program income to the annual CDBG program. Grantees should review all applicable Federal Register notices that establish program income requirements for each CDBG-DR or CDBG-MIT grant, including provisions for transferring program income to the annual CDBG program.

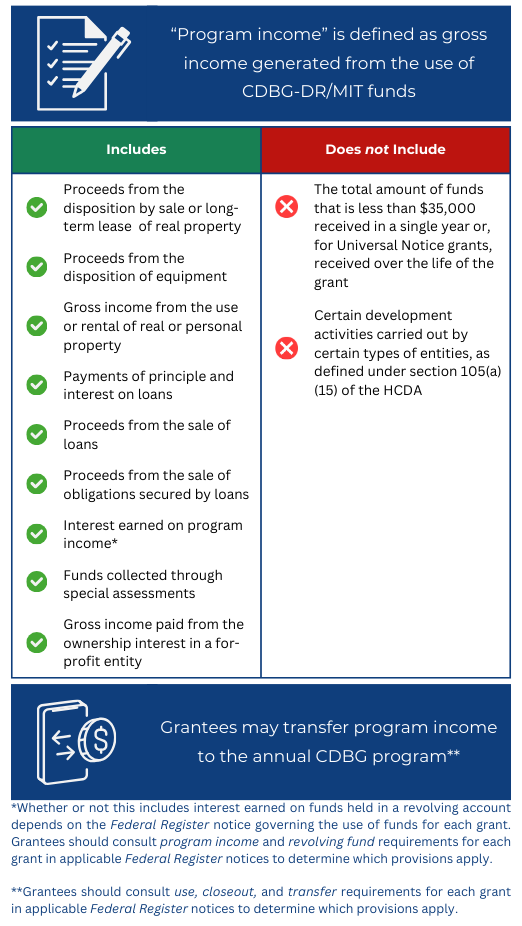

"Program income" is defined as gross income generated from the use of CDBG-DR/MIT funds. This includes the following: Proceeds from the disposition by sale or long-term lease of real property; Proceeds from the disposition of equipment, Gross income from the use or rental of real or personal property, Payments of principle and interest on loans, Proceeds from the sale of loans, Proceeds from the sale of obligations secured by loans, Funds collected through special assessments, Gross income paid from the ownership interest in a for-profit entity , and interest earned on program income.

Note for interest earned on program income, Whether or not this includes interest earned on funds held in a revolving account depends on the Federal Register notice governing the use of funds for each grant. Grantees should consult program income and revolving fund requirements for each grant in applicable Federal Register notices to determine which provisions apply.

Program income does not include: The total amount of funds that is less than $35,000 received in a single year or, for Universal Notice grants, received over the life of the grant, and Certain development activities carried out by certain types of entities, as defined under section 105(a)(15) of the HCDA.

Grantees may transfer program income to the annual CDBG program. Grantees should consult use, closeout, and transfer requirements for each grant in applicable Federal Register notices to determine which provisions apply.

Content current as of July 26, 2024.

- Log in to post comments